Configurable Risk Scoring Models

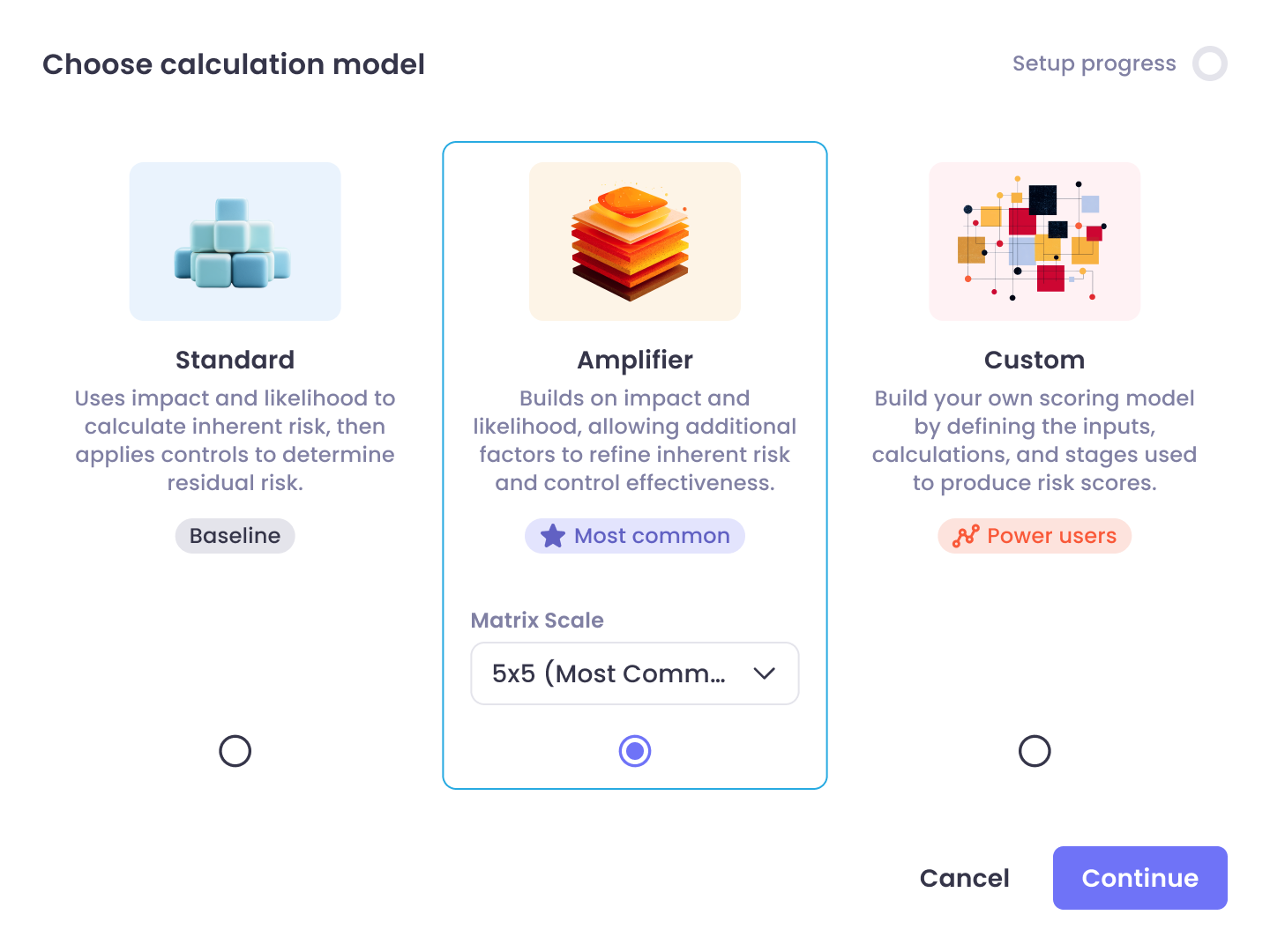

The model selection needed to happen early in setup, but without overwhelming users who'd never thought about model types before. The solution was a guided selection step that presented three clearly labeled options with plain-language descriptions and formula previews. Each option only revealed its configuration needs once selected, keeping the initial screen clean. Users who just needed "standard" could be in and out in seconds. Users building something more complex had a clear path forward.

| Model | Who it's for | Setup experience |

|---|---|---|

| Standard | Teams using impact × likelihood + controls | Defaults first; minimal configuration |

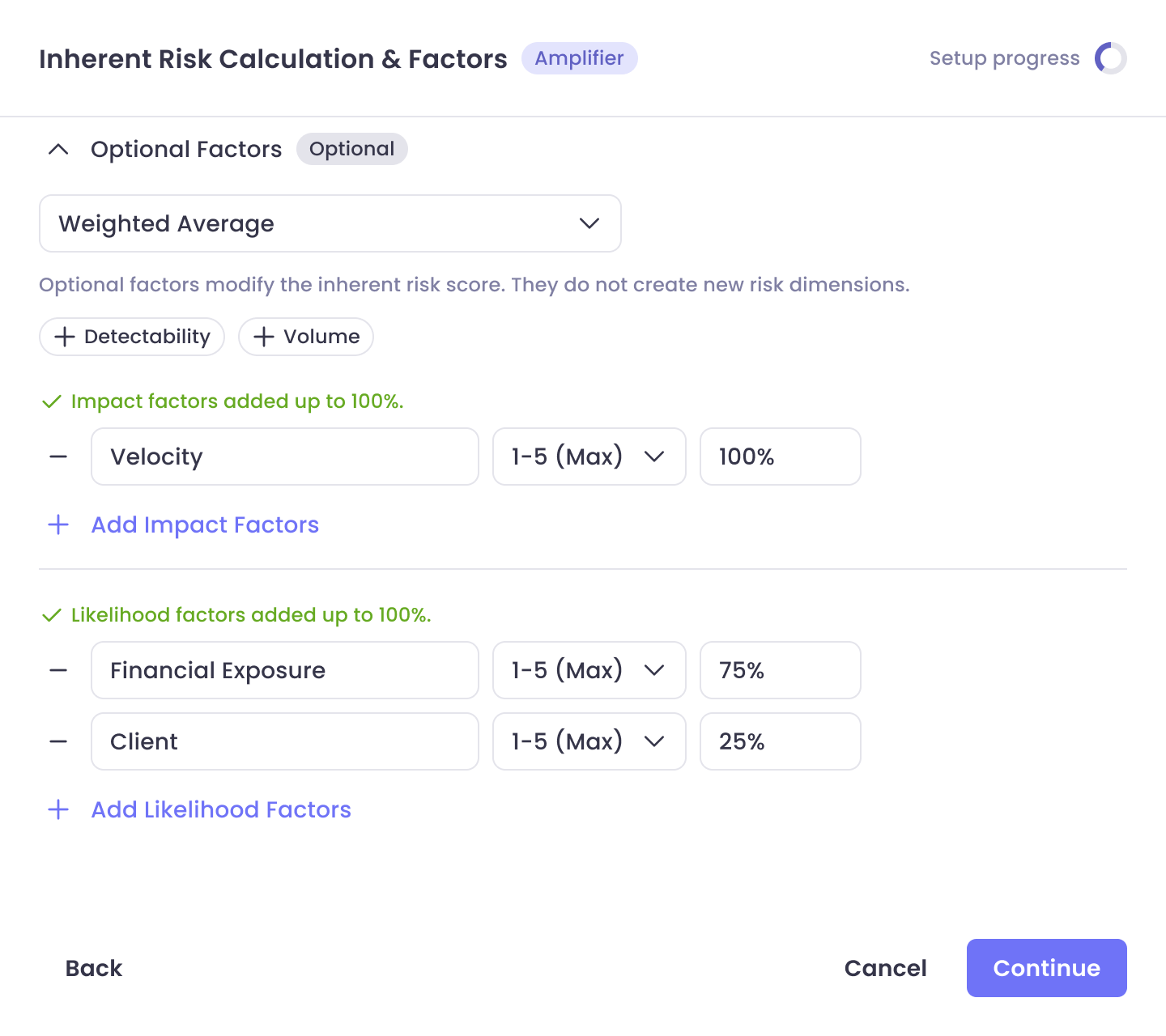

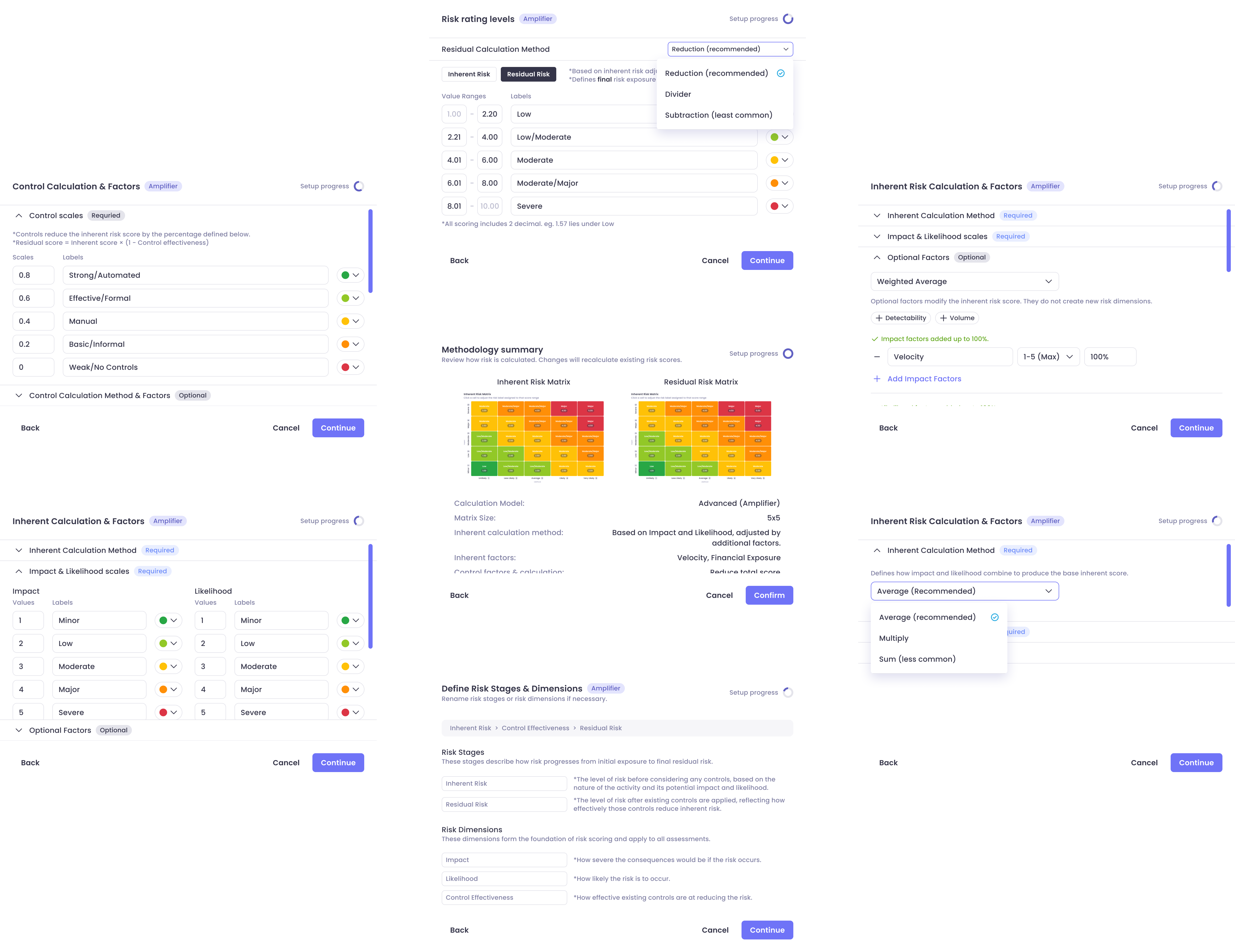

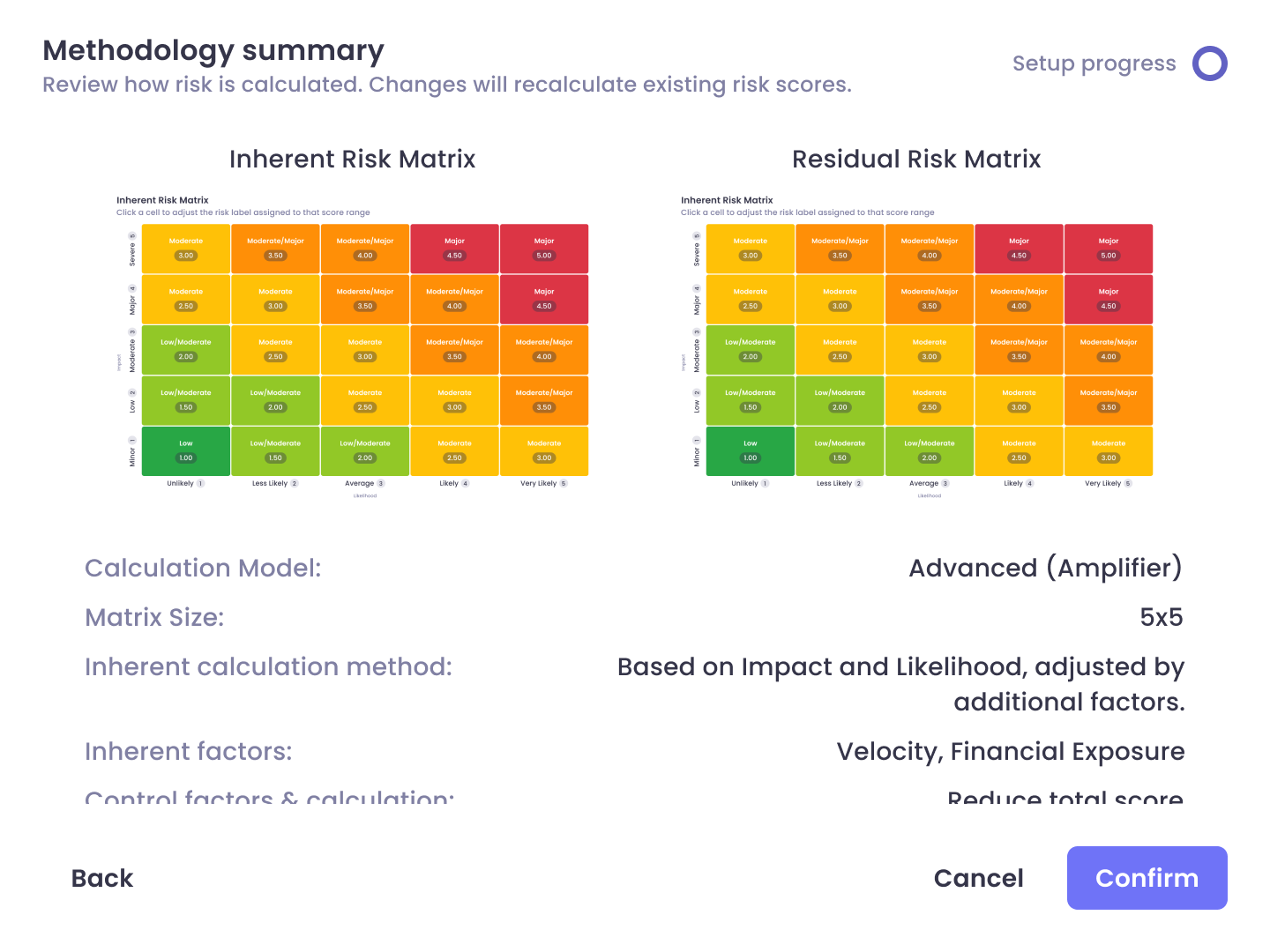

| Amplifier | Teams stacking weighted sub-factors into a roll-up | Guided hierarchy after model pick |

| Custom | Single-dimension focus or non-matrix logic | Dedicated path once selected |